This website is only directed at persons within the UK.

Anthony Marshall trading As Marshall Financial Solutions is an appointed representative of The On-Line Partnership Limited which is authorised and regulated by the Financial Conduct Authority

Business Protection

Cross Option Agreements :

Send Us an enquiry

Do you know how your business would cope if it lost a Key Person?

Protecting you - Saving you Time and Money

The death of a shareholder who is also a director can have a major impact on any business if the company has not made plans for such an event. It is a particular concern for owner/managers of small and medium-sized companies, since the shareholder’s death can potentially give rise to a host of adverse consequences for the business.

Send Us an enquiry

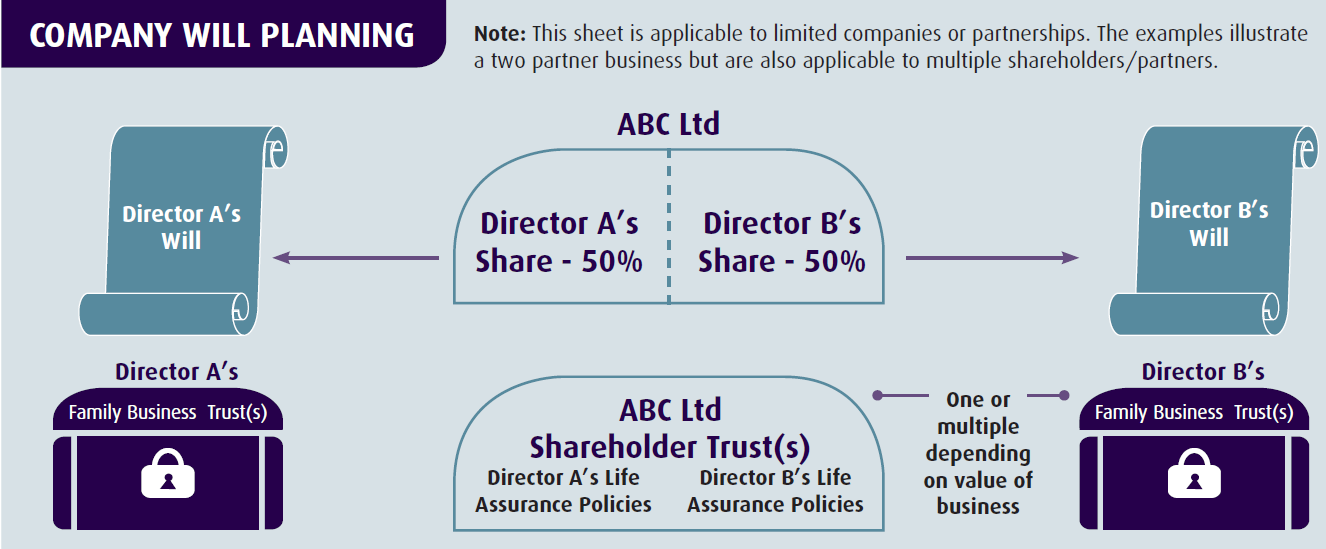

On Director A’s death his share of the business enters his Family Business Trust(s) via his Will. The Life Cover pays out into the Shareholder Trust(s). The surviving Trustees now have the funds to purchase the Deceased’s share and the Cross Option Agreement can be executed.

Cross Option Agreements :

Beneficiaries will now own part of the company which they may not want to run.

Shares in the company are now part of Beneficiaries’ estates and therefore is at risk from Divorce, Remarriage, Bankruptcy and Long Term Care.

If the Beneficiaries decide to sell the business, the proceeds will enter their estates creating a potential IHT liability on their death.

Consequences to Director A’s Beneficiaries

May not want to run the company in partnership with Director A’s Beneficiaries.

May not have the funds to buy out Director A’s share of the business. Note: The effects of the above problems would increase considerably if the company share is a minority holding.

Consequences to Director B

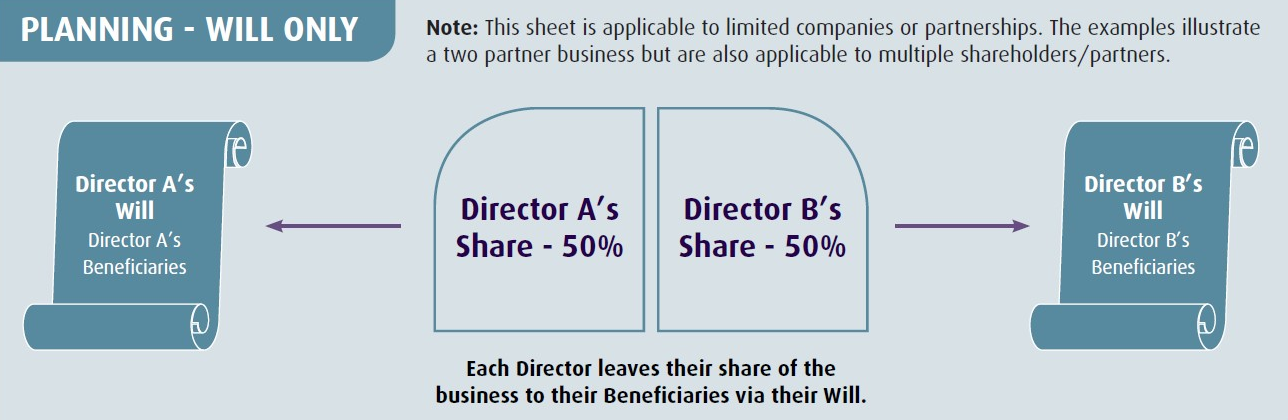

Each Director leaves their share of the business to their respective Family Business Trust(s) via a Business Clause in their Will.

A Cross Option Agreement is established to enable one Director to purchase the other Director’s share of the business in the event of their death.

Life Assurance Policies are taken out in order to fund the purchase of the Deceased Director’s share.

The Life Assurance Policies are assigned to the Shareholder Trust.

Each Life Assurance Policy should not exceed the Nil Rate Band and should be on a Single Life Basis, rather than Joint or on the life of another. The number of Life Assurance Policies and Family Business Trusts required will depend on value of the Business.

TAX & TRUST CORPORATION RESULT OF PLANNING

The cash proceeds from the Life Assurance Plan are now held in Director A’s Family Trust, not the Beneficiaries’ estates. These funds cannot be assessed against anyone for IHT purposes.

The funds are now also protected from the risk of claims from Divorce, Remarriage, Bankruptcy and Long Term Care.

Advantages For Director A’s Beneficiaries

Advantages For Director B

Director B still owns 50% of the company. The other 50% is owned by the Shareholder Trust, of which Director B with his family are both Trustees and Beneficiaries.

- If Director B now wishes to sell the business, only 50% of the sale proceeds will enter his estate and the other 50% will belong to the Trust. - The 50% of sale proceeds owned by the Trust is protected and cannot be assessed against Director B for Inheritance Tax purposes.

The 50% of sale proceeds owned by the Trust is also protected from the risk of claims from Remarriage, Bankruptcy and Long Term Care.

Half of any dividends paid would be to the Shareholder Trust.

These can be distributed to the Beneficiaries in the Trust. Hence the Shareholder Trust can be used as an Income Tax planning tool.

Example of potential Capital Gains Tax savings

If Company Sold: CGT on Trust share = £0 CGT on share held by Director B = £900,000 x 10% = £90,000, compared with a total of £180,000 payable without our planning.

Example of potential Inheritance Tax savings Director A and Director B each own 50% of ABC Ltd which is valued at £1,800,000. Director A dies leaving 50% of the business to his Beneficiaries. The Cross Option Agreement is executed resulting in £900,000 entering the Director A’s Family Business Trusts.

When the Spouse dies the IHT bill on these funds = £0 (compared with a potential bill of £360,000 without our planning). Subsequently, Director B decides to sell the business resulting in £900,000 entering the Shareholder Trust and £900,000 entering his estate.

When Director B dies he leaves a potential IHT bill of 900,000 x 40% = £360,000 (compared with £720,000 without our planning, a saving of £360,000).

With our planning, the potential saving on the Combined IHT bill = £1,080,000 - £360,000 = £720,000

Consequences to Director A’s Beneficiaries

Beneficiaries now have the funds from the Life Family Assurance Policy. These funds are now part of their estates and so will be assessable for Inheritance Tax when they die. These funds are also at risk from claims from Divorce, Remarriage, Bankruptcy and Long Term Care.

Consequences to Director B

3rd Party Claims Will now own 100% of ABC Ltd which is at risk from Divorce, Remarriage, Bankruptcy and Long Term Care. IHT Whilst trading, Business Property Relief is applicable. However if he sells the business, the cash proceeds will then be part of his estate and so will be assessable for Inheritance Tax when he dies. CGT On sale, the growth in Director B’s share has increased and hence more CGT payable than necessary.

Example of potential Capital Gains Tax savings

If Company Sold: CGT on Trust share = £0 CGT on share held by Director B = £900,000 x 10% = £90,000, compared with a total of £180,000 payable without our planning. (See Key Features and Benefits Sheet 10 1/2: Cross Option Agreements)

Example of potential Inheritance Tax savings Director A and Director B each own 50% of ABC Ltd which is valued at £1,800,000. Director A dies leaving 50% of the business to his Beneficiaries. The Cross Option Agreement is executed resulting in £900,000 entering the Director A’s Family Business Trusts.

When the Spouse dies the IHT bill on these funds = £0 (compared with a potential bill of £360,000 without our planning). (See Key Features and Benefits Sheet 10 1/2: Cross Option Agreements) Subsequently, Director B decides to sell the business resulting in £900,000 entering the Shareholder Trust and £900,000 entering his estate.

When Director B dies he leaves a potential IHT bill of 900,000 x 40% = £360,000 (compared with £720,000 without our planning, a saving of £360,000).

(See Key Features and Benefits Sheet 10 1/2: Cross Option Agreements)

With our planning, the potential saving on the Combined IHT bill = £1,080,000 - £360,000 = £720,000

The death of a shareholder who is also a director can have a major impact on any business, if the company has not made plans for such an event. It is a particular concern For owner/managers of small and medium-sized companies, since the shareholder’s death can potentially give rise to a host of adverse consequences for the business.

Beneficiaries will now own part of the company which they may not want to run.

Shares in the company are now part of Beneficiaries’ estates and therefore is at risk from Divorce, Remarriage, Bankruptcy and Long Term Care.

If the Beneficiaries decide to sell the business, the proceeds will enter their estates creating a potential IHT liability on their death.

May not want to run company in partnership with Director A’s Beneficiaries.

May not have the funds to buy out Director A’s share of the business. Note: The effects of the above problems would increase considerably if the company share is a minority holding.

TAX & TRUST CORPORATOPN RESULT OF PLANNING

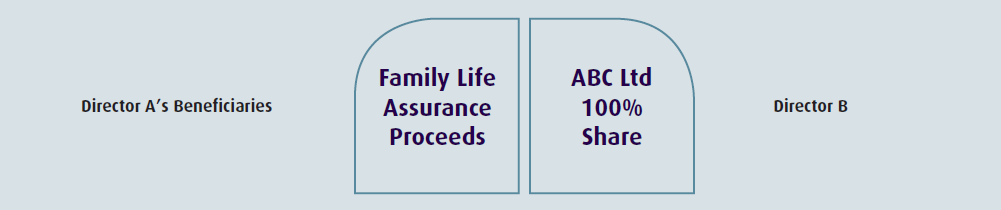

Beneficiaries now have the funds from the Life Family Assurance Policy.

These funds are now part of their estates and so will be assessable for Inheritance Tax when they die. These funds are also at risk from claims from Divorce, Remarriage, Bankruptcy and Long Term Care.

3rd Party Claims Will now own 100% of ABC Ltd which is at risk from Divorce, Remarriage, Bankruptcy and Long Term Care. IHT Whilst trading, Business Property Relief is applicable. However if he sells the business, the cash proceeds will then be part of his estate and so will be assessable for Inheritance Tax when he dies. CGT On sale, the growth in Director B’s share has increased and hence more CGT payable than necessary.

3rd Party Claims Will now own 100% of ABC Ltd which is at risk from Divorce, Remarriage, Bankruptcy and Long Term Care. IHT Whilst trading, Business Property Relief is applicable. However if he sells the business, the cash proceeds will then be part of his estate and so will be assessable for Inheritance Tax when he dies. CGT On sale, the growth in Director B’s share has increased and hence more CGT payable than necessary.

Beneficiaries now have the funds from the Life Family Assurance Policy.

These funds are now part of their estates and so will be assessable for Inheritance Tax when they die.

These funds are also at risk from claims from Divorce, Remarriage, Bankruptcy and Long Term Care.

Each Director leaves their share of the business to their respective Family Business Trust(s) via a Business Clause in their Will.

A Cross Option Agreement is established to enable one Director to purchase the other Director’s share of the business in the event of their death.

Life Assurance Policies are taken out in order to fund the purchase of the Deceased Director’s share.

The Life Assurance Policies are assigned to the Shareholder Trust.

Each Life Assurance Policy should not exceed the Nil Rate Band and should be on a Single Life Basis, rather than Joint or on the life of another. The number of Life Assurance Policies and Family Business Trusts required will depend on value of the Business.

On Director A’s death his share of the business enters his Family Business Trust(s) via his Will. The Life Cover pays out into the Shareholder Trust(s). The surviving Trustees now have the funds to purchase the Deceased’s share and the Cross Option Agreement can be executed.

On Director A’s death his share of the business enters his Family Business Trust(s) via his Will. The Life Cover pays out into the Shareholder Trust(s). The surviving Trustees now have the funds to purchase the Deceased’s share and the Cross Option Agreement can be executed.

Example of potential Capital Gains Tax savings

If Company Sold: CGT on Trust share = £0 CGT on share held by Director B = £900,000 x 10% = £90,000, compared with a total of £180,000 payable without our planning. (See Key Features and Benefits Sheet 10 1/2: Cross Option Agreements)

Example of potential Inheritance Tax savings Director A and Director B each own 50% of ABC Ltd which is valued at £1,800,000. Director A dies leaving 50% of the business to his Beneficiaries. The Cross Option Agreement is executed resulting in £900,000 entering the Director A’s Family Business Trusts.

When the Spouse dies the IHT bill on these funds = £0 (compared with a potential bill of £360,000 without our planning). (See Key Features and Benefits Sheet 10 1/2: Cross Option Agreements) Subsequently, Director B decides to sell the business resulting in £900,000 entering the Shareholder Trust and £900,000 entering his estate.

When Director B dies he leaves a potential IHT bill of 900,000 x 40% = £360,000 (compared with £720,000 without our planning, a saving of £360,000).

With our planning, the potential saving on the Combined IHT bill = £1,080,000 - £360,000 = £720,000

The cash proceeds from the Life Assurance Plan are now held in Director A’s Family Trust, not the Beneficiaries’ estates. These funds cannot be assessed against anyone for IHT purposes. The funds are now also protected from the risk of claims from Divorce, Remarriage, Bankruptcy and Long Term Care.

Director B still owns 50% of the company. The other 50% is owned by the Shareholder Trust, of which Director B with his family are both Trustees and Beneficiaries.

- If Director B now wishes to sell the business, only 50% of the sale proceeds will enter his estate and the other 50% will belong to the Trust.

- The 50% of sale proceeds owned by the Trust is protected and cannot be assessed against Director B for Inheritance Tax purposes.

The 50% of sale proceeds owned by the Trust is also protected from the risk of claims from Remarriage, Bankruptcy and Long Term Care. Half of any dividends paid would be to the Shareholder Trust. These can be distributed to the Beneficiaries in the Trust. Hence the Shareholder Trust can be used as an Income Tax planning tool.

Inheritance Tax Planning, Will Writing, Tax Planning, Trust and estate planning are not regulated by the Financial Coduct Authority.

The plan will have no cash in value at any time, and will cease at the end of the term. if the premiums are not maintained , the cover will lapse.

Source of information : Country Wide Wills & Trusts

Inheritance Tax Planning, Will Writing, Tax Planning, Trust and estate planning are not regulated by the Financial Coduct Authority.

The plan will have no cash in value at any time, and will cease at the end of the term. if the premiums are not maintained , the cover will lapse.

Source of information : Country Wide Wills & Trusts